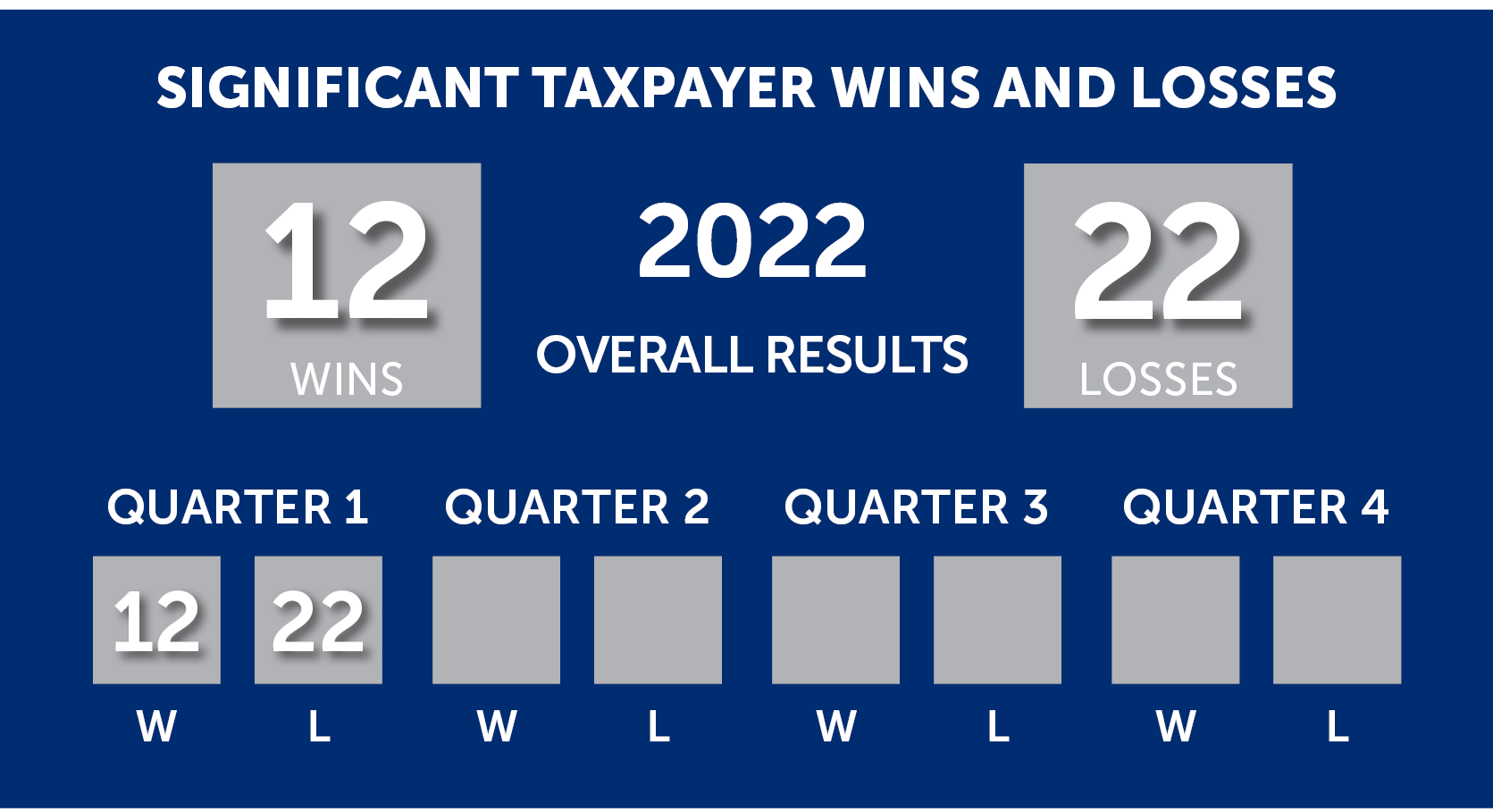

This is the fourth edition of the Eversheds Sutherland SALT Scoreboard for 2023. Since 2016, we have tallied the results of significant taxpayer wins and losses and analyzed those results.

View our Eversheds Sutherland SALT Scoreboard results from the fourth quarter of 2023 now!