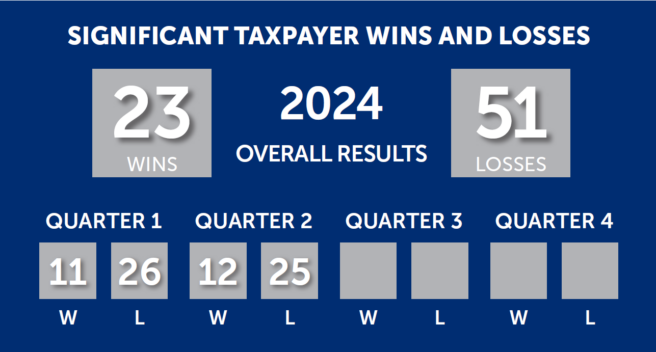

This is the first edition of the Eversheds Sutherland SALT Scoreboard for 2026. For more than a decade, we have tallied the results of what we deem to be the significant taxpayer wins and losses and analyzed those results.

This edition includes discussion of Public Law 86-272 and intercompany transfers, as well as a spotlight