The Massachusetts Supreme Judicial Court has accepted a direct appeal from an internet retailer contesting the Department’s position that the in-state presence of cookies and apps were sufficient to satisfy the physical presence nexus standards in place prior to the US Supreme Court’s decision in South Dakota v. Wayfair, Inc. The Department assessed use tax on the basis that the cookies and apps placed on the devices of Massachusetts-based consumers was sufficient to create physical presence nexus. The Massachusetts Appellate Tax Board disagreed, determining cookies and apps did not satisfy the physical presence standard for pre-Wayfair periods, while also rejecting the Department’s position that Wayfair should be applied retroactively. Despite its victory at the lower level, the taxpayer initiated the direct appeal to the Supreme Judicial Court once the Department filed a notice of appeal to the Massachusetts court of appeals, an intermediate appellate court.

SALT team to present for regional conferences this week

On May 16, Eversheds Sutherland Partner Nikki Dobay will present Basic Unitary/Filing Methods and State and Local Practice Overview during COST’s SALT Basics School in Atlanta, GA. For more information and to register, click here.

On May 17, Eversheds Sutherland attorneys Maria Todorova and Justin Brown will present The Corporate Income Tax Base and Advanced Domestic State Adjustments during COST’s Intermediate/Advanced State Income Tax School in Atlanta, GA. Nikki Dobay will present Gross Receipts Taxes/Modified Gross Receipts Taxes. For more information and to register, click here.

On May 18, Eversheds Sutherland Partner Jonathan Feldman will present Manufacturing/Construction Sales & Use Tax Issues during COST’s Intermediate/Advanced Sales & Use Tax School in Atlanta, GA. For more information and to register, click here.

In addition, the Tax Practice Group is sponsoring TEI Region 10’s 42nd Annual Tax Conference in La Jolla, CA from May 16 to 18. Speakers and topics include:

- Diversity and Inclusion – Maria Todorova

- Audit Panel – Jeff Friedman

- M&A Panel – Maria Todorova

For more information and to register, click here.

Eversheds Sutherland Partner Charlie Kearns will present a Remote Work session during the National Conference of State Legislatures in Seattle, WA on May 18.

Finally, several members of the SALT team will present during the TEI Los Angeles’ Chapter SALT seminar in Hawthorne, CA on May 19. Speakers and topics include:

- 2022 Litigation Round up – Jeff Friedman and Michele Borens

- 2022 SALT Legislative Outlook – Nikki Dobay and John Ormonde

- Local Taxes: Developments in Increasingly-Aggressive Local Taxation – Nikki Dobay and Michele Borens

- Combined Reporting – 80/20’s and Other Issues – Jeff Friedman and Cyavash Ahmadi

- Taxation of Digital Goods and Services – Jeff Friedman and Michele Borens

To register, click here.

A deep dive into the attempt to expand the False Claims Act

In this episode of the SALT Shaker Podcast policy series, host and Eversheds Sutherland Partner Nikki Dobay welcomes back Stephanie Do, Senior Tax Counsel for the Council On State Taxation (COST), for a discussion about two recent proposals to expand the False Claims Acts in Connecticut and New York.

As our listeners know, most states have a false claims act that is modeled after the federal False Claims Act, which includes a bar against tax claims. Stephanie provides an overview of False Claims Act presence in the states and the potential for expansion in some states to include tax matters. Stephanie and Nikki discuss a Connecticut bill from this year’s session that sought to expand the state’s False Claims Act and how the bill was stopped (for now).![]()

Nikki and Stephanie then discuss how these expansions fit into the larger policy space, and how False Claims Act expansion is faring in New York in this legislative session.

Nikki’s surprise non-tax question this week involves Mother’s Day – what is your favorite Mother’s Day tradition?

The Eversheds Sutherland SALT team has been engaged in state tax policy work for years, tracking tax legislation, helping clients gauge the impact of various proposals, drafting talking points and rewriting legislation. Partner Nikki Dobay, who has an extensive background in tax policy, hosts this series, which is focused on state and local tax policy issues.

Questions or comments? Email SALTonline@eversheds-sutherland.com. You can also subscribe to receive our regular updates hosted on the SALT Shaker blog.

Listen now:

Subscribe for more:

SALT trivia – May 11, 2022

Calling all trivia fans! Don’t miss out on a chance to show off your SALT knowledge!

We will award prizes for the smartest (and fastest) participants.

This week’s question: Which ruling recently found that online learning plans were not taxable digital goods?

E-mail your response to SALTonline@eversheds-sutherland.com.

The prize for the first response to today’s question is a $25 UBER Eats gift card. Answers will be posted on Saturdays in our SALT Shaker Weekly Digest. Be sure to check back then!

Wisconsin marketplace providers responsible for collecting premier resort area taxes

The Wisconsin Department of Revenue recently published updated guidance that states that marketplace providers are responsible for the collection and remittance of the Wisconsin premier resort taxes. For purposes of collection and remittance responsibilities, a marketplace provider in Wisconsin is a person who facilitates a retail sale on a seller’s behalf by listing or advertising the seller’s products and services, and who processes the payment. Wisconsin has eight premier resort areas, and every sale subject to the state sales tax is also subject the premier resort area tax if the sale takes place in one of those eight areas and the seller is classified under one of the listed Standard Industrial Classification (SIC) codes.

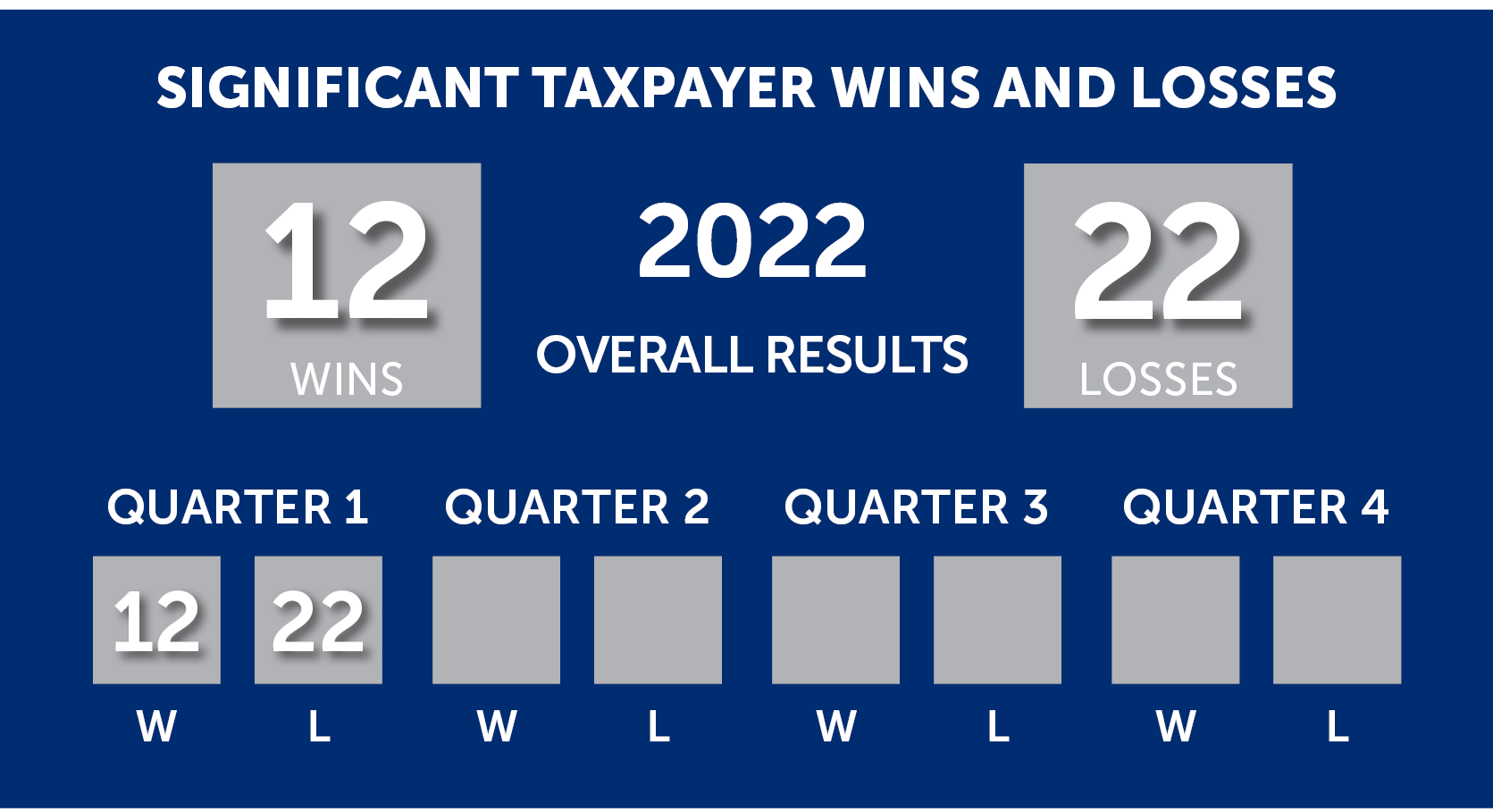

SALT Scoreboard – First Quarter 2022

This is the first edition of the Eversheds Sutherland SALT Scoreboard for 2022. Since 2016, we have tallied the results of significant taxpayer wins and losses and analyzed those results.

View our Eversheds Sutherland SALT Scoreboard results from the first quarter of 2022 now!

What’s the skinny on the MTC?

In this week’s episode of the SALT Shaker Podcast policy series, our typical format is switched up! Eversheds Sutherland Associate Jeremy Gove tries his hand in the policy space and interviews Partner Nikki Dobay about the latest updates from the MTC.

The MTC just held its spring meetings in Albuquerque, New Mexico in April, including the Uniformity Committee meeting on April 20. (You can read some highlights from the meeting in our full legal alert.) ![]()

Jeremy and Nikki cover the ongoing developments with the MTC’s recently updated statement on PL 86-272, how the statement is being received, and taxpayers’ concerns with the MTC’s proposed interpretation of that federal law. They also highlight Nikki’s efforts at working with the Committee to establish a universal power of attorney form, and wrap up by touching on the Committee’s current uniformity projects on state taxation of partnerships and taxation of digital goods.

Their discussion concludes with a surprise, nontax question – if you were any type of body of water, what would you be, and why?

The Eversheds Sutherland SALT team has been engaged in state tax policy work for years, tracking tax legislation, helping clients gauge the impact of various proposals, drafting talking points and rewriting legislation. Partner Nikki Dobay, who has an extensive background in tax policy, hosts this series, which is focused on state and local tax policy issues.

Questions or comments? Email SALTonline@eversheds-sutherland.com. You can also subscribe to receive our regular updates hosted on the SALT Shaker blog.

Listen now:

Subscribe for more:

Years in the making: New York issues two sets of “final draft” corporate tax reform regulations

On April 29, 2022, the New York State Department of Taxation and Finance issued two sets of “final draft” regulations relating to the corporation franchise tax reform that took effect for tax years beginning on or after January 1, 2015. Since the sweeping corporate tax reform was enacted, the Department has published a series of proposed updates to the Article 9-A corporation franchise tax regulations, but the two sets of regulations issued on April 29 are the first to be identified as “final drafts.” One set relates to regulation Parts 1 – 3 (definitions, nexus, losses, etc.), and the other set relates to regulation Parts 5 – 10 (tax credits, reports, assessments, etc.). The Department has indicated that a third set of “final draft” regulations, regarding Part 4 (apportionment), will be published in “summer 2022.”

According to the Department’s website, the Department “intends to begin the State Administrative Procedure Act (SAPA) process to formally propose and adopt these regulations” this fall, and requests comments on the two sets of draft regulations by June 30, 2022.

The Department’s website continues to include a “reminder” that “these draft regulations are not yet final and should not be relied upon.”

The draft regulations can be found on the Department’s website here.

Minnesota Tax Court rules credit card processing fee taxable

The Minnesota Tax Court ruled that a separately stated surcharge covering credit card processing fees was subject to sales tax. The taxpayer, a sole proprietor, operates vacation rental properties that are held out for booking either directly through the taxpayer or through third-party marketers. The taxpayer charges a 4% separately stated surcharge for reservations booked directly with him as a reimbursement of his credit card fees. The taxpayer had not collected sales tax on the surcharge. The Tax Court concluded that the credit card surcharge is included within the broad statutory definition of “sales price,” and thus is subject to sales tax. The Tax Court reasoned that the surcharge is an expense of the seller that cannot be deducted from the sales price and that the fee did not qualify for the exception for “carrying charges from credit extended on the sale of personal property or services.”

SALT trivia – May 4, 2022

Calling all trivia fans! Don’t miss out on a chance to show off your SALT knowledge!

We will award prizes for the smartest (and fastest) participants.

This week’s question: Who was our April 2022 SALT Pet of the Month?

E-mail your response to SALTonline@eversheds-sutherland.com.

The prize for the first response to today’s question is a $25 UBER Eats gift card. Answers will be posted on Saturdays in our SALT Shaker Weekly Digest. Be sure to check back then!