The Supreme Court of Ohio held that gross receipts from a taxpayer’s services performed out-of-state had situs with Ohio for purposes of the state’s commercial activity tax (CAT) because the benefit of the services was received in Ohio. The taxpayer provided dialysis services to patients in Ohio. To support the dialysis business, the taxpayer and

Ohio Board of Tax Appeals holds motor vehicle sales sourced outside of Ohio for CAT

The Ohio Board of Tax Appeals held that automobile dealers were not subject to the Ohio Commercial Activity Tax (CAT) on their sales of motor vehicles because the purchase, receipt, and delivery of the vehicles took place entirely outside of Ohio. The Department of Taxation assessed the dealers, which were located in West Virginia, for

SALT Scoreboard – Third Quarter 2024

This is the third edition of the Eversheds Sutherland SALT Scoreboard for 2024. Since 2016, we have tallied the results of significant taxpayer wins and losses and analyzed those results.

View our Eversheds Sutherland SALT Scoreboard results from the third quarter of 2024 now!

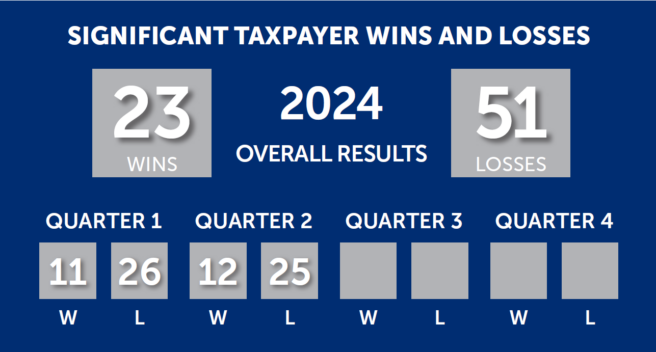

SALT Scoreboard – Second Quarter 2024

This is the second edition of the Eversheds Sutherland SALT Scoreboard for 2024. Since 2016, we have tallied the results of significant taxpayer wins and losses and analyzed those results.

View our Eversheds Sutherland SALT Scoreboard results from the second quarter of 2024 now!

South Carolina Court holds receipts from mortgage activities and credit cards should be sourced to state

The South Carolina Administrative Law Court upheld a bank tax assessment that was based on adjustments made by the Department of Revenue to a taxpayer’s sales factor and tax base. The taxpayer, a national bank, offered a range of banking and trust services, and generated income by providing residential mortgages and other loans, and issuing

Oregon Supreme Court holds prebook orders not subject to PL 86-272 protection

The Oregon Supreme Court recently held that an out-of-state tobacco manufacturer’s acceptance of prebook orders precluded it from availing itself of Public Law 86-272 protection against the imposition of the state’s corporate excise tax. In 1959, the U.S. Congress passed P.L. 86-272, which prohibits states from imposing a net income tax when the business’s only

Washington Court of Appeals holds sales of pre-paid telephone airtime subject to municipal utility tax

The Washington Court of Appeals held that the sales of pre-paid telephone airtime purchased from third-party cellular networks by a business (Taxpayer) and resold to individual customers and retailers were subject to the City of Renton’s municipal utility tax.

The utility tax was imposed on the privilege of conducting a “telephone business” within city limits

A family affair: Alabama Tax Tribunal holds parent company cannot use NOLs for indirectly-owned subsidiary

The Alabama Tax Tribunal held that a parent company could not use its losses to offset the income of a bank that it owned through an intermediate holding company for the purposes of the state’s Financial Institution Excise Tax (FIET). The applicable law allowed financial institution members of a commonly owned controlled group to file

SALT Scoreboard – First Quarter 2024

This is the first edition of the Eversheds Sutherland SALT Scoreboard for 2024. Since 2016, we have tallied the results of significant taxpayer wins and losses and analyzed those results.

View our Eversheds Sutherland SALT Scoreboard results from the first quarter of 2024 now!

Not so fast: Illinois fuel distributor partly liable for taxes on fuel transfers to affiliates

On March 22, 2024, the Appellate Court of Illinois issued a split decision in a case involving local fuel taxes transferred by a fuel distributor to affiliates that operated gas stations in Cook County, Illinois.

Under Cook County’s local fuel tax ordinance, distributors must pay a 6 cent per gallon tax on fuel sold to