The District of Columbia Office of Administrative Hearings held that the two financial institution subsidiaries of Petitioner, a credit and charge card issuer company, should have included in their payroll factor denominator only the payroll attributable to the financial institution entities. In other words, when calculating their payroll factor, Petitioner’s financial institution subsidiaries should have

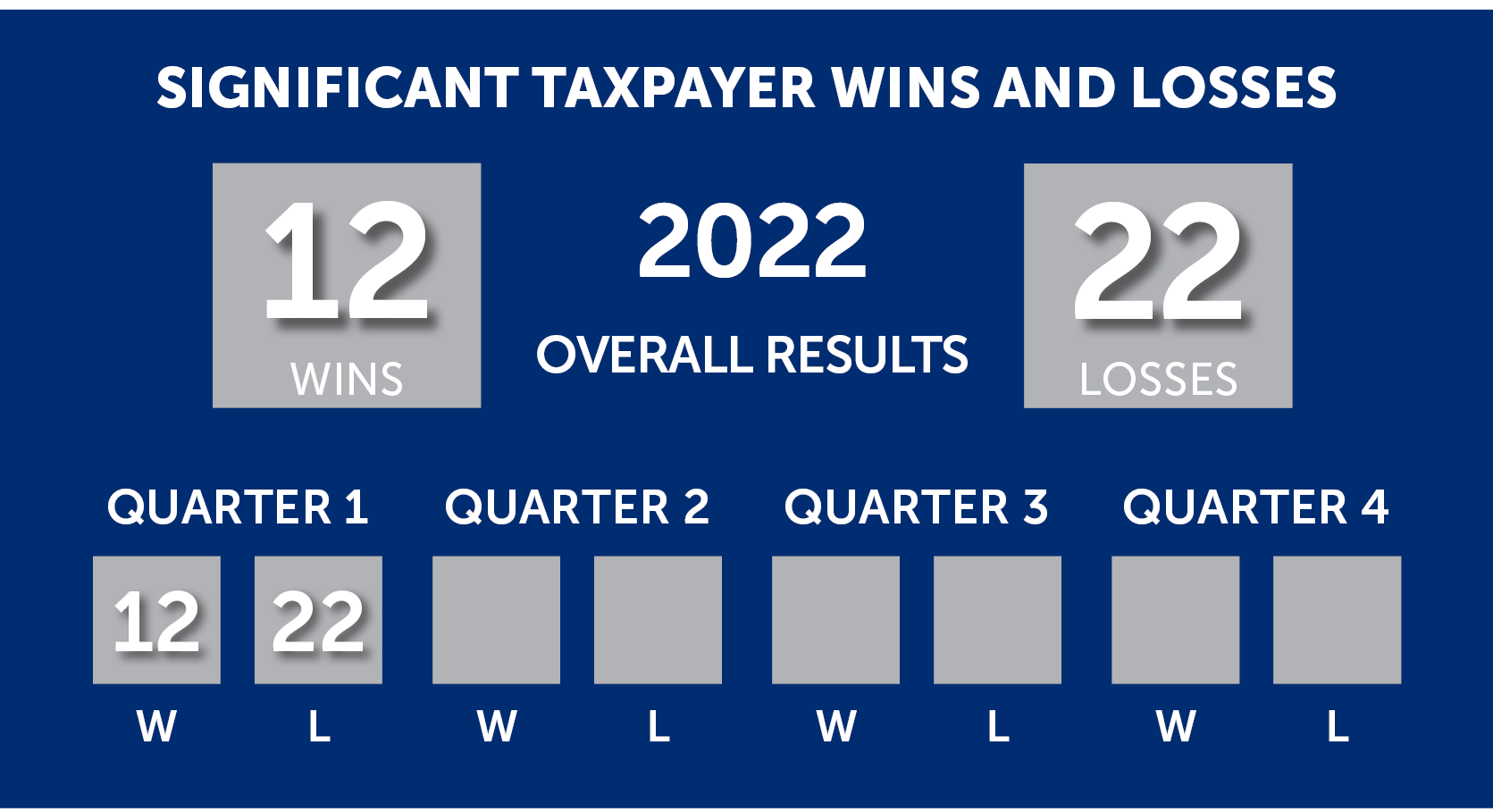

SALT Scoreboard – Second Quarter 2022

This is the second edition of the Eversheds Sutherland SALT Scoreboard for 2022. Since 2016, we have tallied the results of significant taxpayer wins and losses and analyzed those results.

View our Eversheds Sutherland SALT Scoreboard results from the second quarter of 2022 now!

Washington Department of Revenue finds sales tax must be collected on sales of renewable energy equipment

The Washington Department of Revenue upheld a retail sales tax assessment on a taxpayer who failed to collect retail sales tax on sales to a renewable energy company. The taxpayer stated that it did not collect tax on certain sales because it believed that the energy company qualified for the exemption provided by Wash. Rev.

Booked! Montana Supreme Court finds resort services fee decision is here to stay

The Supreme Court of Montana affirmed a lower court’s determination that a taxpayer was liable for accommodations sales tax on its resort service fees, but did not owe accommodations sales tax for forfeited guest deposits or lodging facilities use tax on its resort service fees. The taxpayer, Boyne USA, Inc. owns and operates Big Sky

Blame the manager: Company that arranges, manages brand displays is a retailer for Washington B&O and retail sales tax purposes

On April 25, the Washington Court of Appeals held that a company that arranges and manages displays for installation and placement in multiple retail brands’ stores through subcontractors was subject to the state’s retailing business and occupation tax (the “B&O tax”) and retail sales tax as a retailer making retail sales, rather than a provider

SALT Scoreboard – First Quarter 2022

This is the first edition of the Eversheds Sutherland SALT Scoreboard for 2022. Since 2016, we have tallied the results of significant taxpayer wins and losses and analyzed those results.

View our Eversheds Sutherland SALT Scoreboard results from the first quarter of 2022 now!

No Maryland sales and use tax exemption for for-profit company’s purchases made for non-profit hospitals

The Maryland Court of Appeals held that a for-profit company’s purchases for non-profit hospitals were subject to Maryland’s sales and use tax because there was no agency relationship between the company and the hospitals, and even if an agency relationship existed, that alone would not entitle the for-profit company to an exemption.

Johns Hopkins Health

Prepare for takeoff: Minnesota’s minimum fee is partially preempted by federal law prohibiting taxation of airline gross receipts

The Minnesota Tax Court ruled that the federal Anti-Head Tax Act (AHTA) preempts using Alaska Airlines’ gross receipts when calculating the Minnesota Franchise Tax Minimum Fee. The AHTA prohibits states from taxing gross receipts from air commerce or transportation. Minnesota’s Minimum Fee, imposed on taxpayers exercising a corporate franchise in the state, is calculated based

Rocky road for bad debts: Colorado Court denies credit to finance company

The Colorado Court of Appeals held that sales tax bad debt credits may not be claimed by a financial company that issued private label credit cards. As a private label retail credit card issuer, Capital One financed purchases made by its cardholders. Under the terms of its agreements with retailers, Capital One financed purchases made

SALT Scoreboard – Fourth Quarter 2021

This is the fourth edition of the Eversheds Sutherland SALT Scoreboard for 2021. Since 2016, we have tallied the results of significant taxpayer wins and losses and analyzed those results.

View our Eversheds Sutherland SALT Scoreboard results from the fourth quarter of 2021 now!